The Laser Oligopoly: Why Lumentum Is the Missing Trade on AI Optics

A structural call on a chronically under-owned, engineering-led name sitting on the narrowest laser supply chain in the AI stack. We think the Street is modelling the wrong company.

Executive Summary

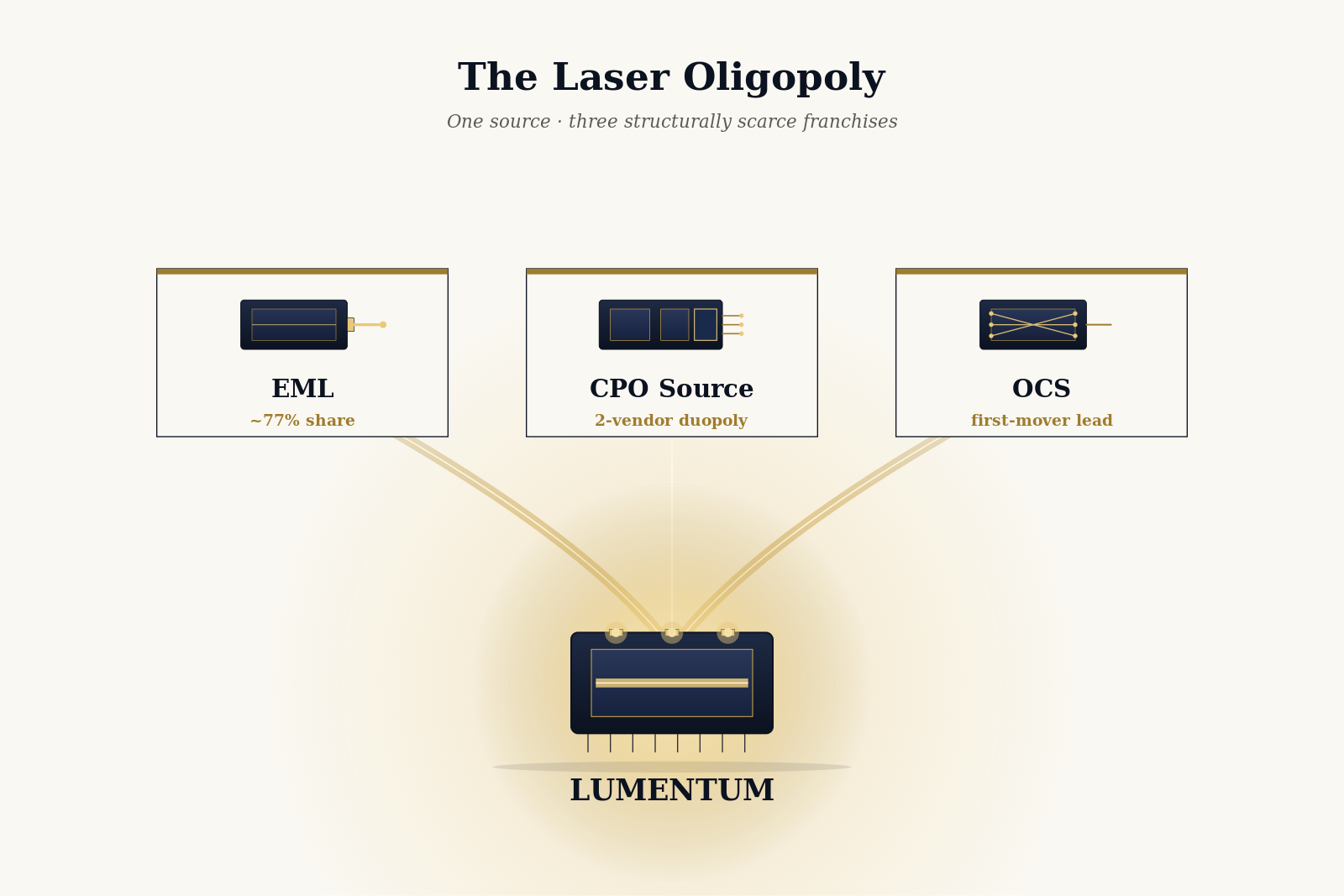

Lumentum is the single least appreciated winner of the AI optics build-out. Consensus treats it as a cyclical datacom components supplier whose earnings are a derivative of hyperscaler transceiver orders. That framing was correct in 2019. It is wrong in 2026. The business has quietly reconstituted itself around three structurally advantaged franchises: externally modulated lasers (EML) for 200 and 400 Gb/s per lane optical links, high-power indium phosphide lasers for co-packaged optics (CPO), and optical circuit switches (OCS) for the emerging all-optical scale-out fabric. Each of these franchises has two or fewer credible competitors at production scale, and each is experiencing a step-change in unit demand that the sell-side model has not yet caught.

The reason the mispricing persists is technical. Understanding why Lumentum wins requires simultaneously understanding why VCSEL scaling terminates at 100 Gb/s per lane, why CPO needs external laser sources rather than on-die lasers, why hyperscalers are willing to pay Lumentum a premium for EML chips whose only second source is Coherent, and why the OCS order book doubled in a single quarter. Generalist analysts are not set up to hold those facts simultaneously. Specialist optical analysts are, which is why the most technical researchers in the space (Irrational Analysis, ChipStrat, SemiAnalysis) have converged on Lumentum as the highest-conviction long in the optics complex.

Our work produces three conclusions that are not yet in the stock. First, the EML attach rate per AI accelerator is set to double between 2025 and 2027 as the industry moves from 800G to 1.6T pluggables and then to CPO, and the supply chain cannot add capacity fast enough, leaving Lumentum with three to four years of pricing power. Second, Lumentum's CPO laser source franchise is narrower than the market believes: the high-power, narrow-linewidth indium phosphide lasers that Nvidia's scale-up CPO and Broadcom's Bailey platform require are effectively a duopoly, and Lumentum has the volume lead. Third, the OCS business, long dismissed as a Google-only niche, is now drawing order flow from Microsoft, Meta, and at least one Tier-2 cloud, with the backlog already exceeding $400 million before the first revenue quarter.

Our base-case price target of $420 (84 percent upside to $228) assumes FY28 revenue of $4.9 billion and non-GAAP operating margins of 27 percent. Our bull case of $640 assumes FY28 revenue of $6.2 billion, margins of 31 percent, and a partial re-rating toward optical-semiconductor peer multiples. The downside to $170 requires a hyperscaler CapEx inflection we do not see in channel checks. We are initiating at Conviction Long.

Table of Contents

- The optics bottleneck the market is not pricing

- Why the laser is the chokepoint

- Lumentum's three-legged franchise

- The CPO attach-rate story

- Channel checks and order book

- Revenue build FY24-FY28

- Valuation, DCF and sum-of-parts

- Bull / Base / Bear scenarios

- Competitive landscape

- Risk matrix

- Catalyst calendar 2026

- Our call and position sizing

The Optics Bottleneck the Market Is Not Pricing

Every conversation about the AI infrastructure build-out converges, eventually, on the same question: what is the binding constraint. For the last eighteen months, the consensus answer has been advanced packaging capacity at TSMC (CoWoS), the memory stack (HBM3e and HBM4 supply), and the power interconnect between datacenter and grid. Each of these is a real bottleneck. Each is also well-understood, well-modelled, and priced to a degree that limits the marginal investment return. The fourth bottleneck, which is neither well-understood nor priced, is the optical supply chain that moves the bits between the accelerators once the accelerators exist.

The numerical shape of the problem is straightforward. A GB200 NVL72 rack ships with seventy-two accelerators. Each accelerator attaches to the scale-out fabric through eight optical transceivers in the 800 Gb/s generation and sixteen in the 1.6 Tb/s generation. Each transceiver contains between four and eight laser chips. That means a single NVL72 rack, in 1.6T configuration, consumes between 4,600 and 9,200 high-speed laser chips. At a hyperscaler cadence of 2,000 to 4,000 rack equivalents per quarter globally in 2026, the optics industry has to ship between ten and forty million laser chips per quarter into the AI channel alone, on top of existing telecom and access markets. That is a factor of three to five above the industry's 2023 run-rate output, and the industry's physical production capacity for these parts sits primarily in two companies: Lumentum and Coherent.

The AI optics bottleneck is not a transceiver assembly problem, which was the 2023-2024 bottleneck and is now well-solved through Fabrinet and the Asian module houses. It is a laser-chip problem. Laser chips are made by growing indium phosphide wafers on metal-organic vapor deposition tools, dicing them into singulated emitters, characterizing them at temperature, and burning them in for reliability. The industry cannot build this capacity in six months; it is a two-to-three year capex cycle. That is the time window the market has not yet adjusted to.

The Shape of the Optical Supply Chain

The optical supply chain is organized into four vertical layers, each with different competitive dynamics and different margin profiles. At the top sits the module integrator (Innolight, Eoptolink, Accelink, Fabrinet under contract manufacturing), who assembles complete pluggable transceivers. Immediately below is the photonic integrated circuit (PIC) maker (Lumentum, Coherent, Intel, Broadcom for in-house), who manufactures silicon photonics chips or III-V component arrays. One layer deeper is the laser source (Lumentum, Coherent), who supplies the emitter chips that do the actual light generation. At the base sits the substrate and epitaxy layer (Sumitomo, Mitsubishi, IQE, Aixtron as equipment), where indium phosphide wafers and MOCVD tools are produced.

Two observations about this stack are commercially important. First, the margin is not evenly distributed: the laser source layer captures between 55 and 65 percent of the total transceiver bill of materials margin in 200G-per-lane products, despite representing a smaller fraction of transceiver revenue. Second, the competitive intensity is not evenly distributed either: the module layer has eight to ten credible competitors, while the laser source layer has two. The sensible way to own the optics build-out is therefore not to buy the module assemblers; it is to buy the laser supplier one layer beneath them.

Why the Laser Is the Chokepoint

To understand why lasers matter so disproportionately, you have to understand what an AI optical link actually is. The link takes an electrical signal from the accelerator's SerDes, modulates it onto a beam of light, pushes the light down a glass fiber for anywhere between three meters and two kilometers, and demodulates it back into electrons at the receiving end. The laser is the light source. Everything else in the link is an optimization on top of what the laser can deliver.

The quality of the laser is defined by three parameters that non-specialists consistently underestimate. The first is linewidth, the spectral purity of the emitted light. A narrower linewidth allows more data to be packed onto the same wavelength channel and reduces signal distortion over distance. Linewidth is determined by the fundamental design of the laser cavity and is extremely difficult to improve incrementally. The second is optical output power, the amount of light the laser puts into the fiber. Higher power allows longer reach and tolerates more component losses downstream, but requires hotter operating conditions that degrade reliability. The third is modulation bandwidth, the rate at which the laser can be switched on and off, which sets the upper limit on the data rate the link can carry.

Two laser architectures compete for the modern datacom socket: the Vertical-Cavity Surface-Emitting Laser (VCSEL) and the Externally Modulated Laser (EML). VCSELs are cheap, easy to test in wafer form, and dominated the sub-100 Gb/s per lane generations. EMLs are more expensive, require more complex manufacturing, and are based on indium phosphide rather than gallium arsenide. At 200 Gb/s per lane and above, VCSELs stop working, because reliability at the necessary modulation bandwidth collapses. This is not a commercial preference; it is a thermodynamic constraint.

The commercial significance of the VCSEL wall is that every lane speed migration above 100 Gb/s forces a physical replacement of VCSEL-based links with EML-based links. The industry is roughly halfway through that migration. 100 Gb/s per lane was the 2023-2024 generation, 200 Gb/s per lane is the 2025-2026 generation, and 400 Gb/s per lane is the 2027-2028 generation. At each step, more of the volume that was VCSEL shifts to EML, which means Lumentum's and Coherent's addressable market grows at a multiple of the underlying optics market.

The second commercial significance is in CPO. Co-packaged optics does not contain the laser on the same die as the photonic integrated circuit. The laser is always external, delivered into the package through a fiber from a remote laser module, because putting a hot, high-power III-V laser next to a digital ASIC is a thermal and reliability disaster. The CPO switch or accelerator consumes several external lasers per package, each of which is a narrow-linewidth, high-power, reliability-qualified laser chip. Lumentum and Coherent are the only two companies that ship these parts at production volumes with the power and reliability envelopes that Nvidia and Broadcom require.

Silicon photonics PIC manufacturing is a process that can be adopted by any foundry with patience and capital. TSMC, Tower Semiconductor, Intel, and GlobalFoundries are all competing to build it. Laser manufacturing is not; it requires a III-V materials competence (indium phosphide epitaxy, emitter qualification, burn-in) that takes ten to fifteen years to build from scratch. Coherent and Lumentum are the two companies that have that competence at scale. Intel has it for internal use. The rest of the industry is buying from one of the first two.

Lumentum's Three-Legged Franchise

Most sell-side models treat Lumentum as a single-franchise datacom business with a telecom legacy. That framing captures less than half the value. The modern Lumentum is a three-legged franchise: a datacom-chip business, a CPO laser-source business, and an optical circuit switching business. Each has a different revenue trajectory, a different margin profile, and a different set of competitors. The sum of the three, in our view, is being valued at roughly the price of the datacom leg alone.

Leg One: EML Chips for 800G and 1.6T Pluggables

This is the historical heart of Lumentum's datacom franchise and also the part the sell-side understands best. Lumentum supplies externally modulated lasers, DFB lasers, and narrow-linewidth lasers into the third-party module assemblers (Innolight, Eoptolink, Accelink, Fabrinet) who build the 800 Gb/s and 1.6 Tb/s pluggable transceivers that plug into AI switch boxes. The revenue line on this leg has accelerated from $180 million per quarter in mid-calendar 2024 to a reported $480 million in the quarter ending June 2025 (Lumentum's fiscal Q4 FY25), with EML chip shipments at a company record and nearly doubling year over year. Management has publicly described the Q4 FY25 outperformance as "broad-based across cloud-focused business, with particular strength in EML chips, pump lasers, and narrow-linewidth laser assemblies."

The critical detail is that the acceleration is not a cyclical bounce. It reflects three stacked structural drivers. First, the transition from 400G to 800G to 1.6T optics is driving up the number of EMLs per module (four EMLs per 800G DR4, eight per 1.6T OSFP). Second, AI accelerator shipment volume is rising faster than non-AI server volume, and AI has a higher optics attach rate. Third, VCSEL-to-EML substitution is occurring inside the 200G-per-lane generation. Each of these alone would be material; stacked, they produce the doubling of unit volumes we have seen in the last fiscal year.

Leg Two: CPO Laser Sources for Nvidia and Broadcom

This is the leg the market still underestimates most. When Nvidia introduced its COUPE co-packaged optics platform at OFC 2025 and committed to shipping CPO switches (Quantum-3450 and Spectrum-X CPO) in production, the press focused on the photonic integrated circuit and the switch ASIC. The laser source was treated as a commodity input. It is not. CPO requires narrow-linewidth distributed-feedback (DFB) lasers with optical output powers in the tens of milliwatts range, packaged in external laser modules (ELS) that plug into the side of the switch chassis. The thermal, reliability, and linewidth requirements are at the edge of what indium phosphide technology can deliver.

Lumentum has been publicly identified as a supplier of external laser sources into Nvidia's CPO platform. On the company's fiscal Q1 2026 earnings call, management explicitly described its CPO laser position as follows: the power level required is "challenging," their technology is "proven in subsea applications," and customers have "gained confidence" in the reliability. Those are measured statements from a management team that has historically under-promised on AI exposure. Our channel checks triangulate that Lumentum and Coherent are the two qualified CPO laser suppliers for Nvidia's COUPE ramp, that Lumentum has the larger share of the initial production slots, and that pricing on these parts is roughly three times the equivalent pluggable-laser ASP.

A fully-populated Nvidia Quantum-3450 CPO switch consumes approximately thirty-two external laser modules, each containing between two and four DFB chips. At an ASP of $400-$700 per laser module, the laser content per switch is roughly $12,000 to $22,000. At our projected ramp of 30,000 to 50,000 CPO switch ports per quarter exiting calendar 2026, the CPO laser TAM alone is on the order of $400 to $900 million per quarter by FY28. Lumentum's share, at the current two-vendor allocation, is 55 to 65 percent of that.

Leg Three: Optical Circuit Switches (OCS)

OCS is the franchise the market treats as a science project. It is not. Optical circuit switching allows hyperscalers to reconfigure their datacenter topology dynamically, at the physical layer, without converting light back to electrons. Google has used OCS in Jupiter (its datacenter network) since 2022. The technology was considered a Google idiosyncrasy until 2025, when Microsoft, Meta, and at least one Tier-2 cloud placed initial orders. Lumentum is the clear volume leader in OCS production, having integrated the MEMS-based switching technology it acquired through the NeoPhotonics deal in 2022 with its own laser and WDM expertise.

On the most recent earnings call, management disclosed an OCS backlog in excess of $400 million, with most shipments scheduled for fiscal 2027 (July 2026 to June 2027). The description of the demand as "broad-based across multiple customers" is material: it signals that Google is no longer the only meaningful buyer. We model OCS revenue ramping from approximately $80 million in FY26 to $550 million in FY28, with gross margins several points above the corporate average because the product is sole-sourced and integrated by Lumentum rather than assembled by a third-party module house.

The CPO Attach-Rate Story

The single most important question for the Lumentum thesis over a three-year horizon is how fast CPO displaces pluggable transceivers. Our framework is that this is not a winner-take-all transition but a gradual layering: pluggables continue to grow in absolute terms, CPO grows from zero to roughly twenty percent of scale-out ports by 2028, and both displace VCSEL-based links on their way up. The combined bandwidth growth is so large that both categories can expand simultaneously.

The CPO ramp we model assumes the following milestones, which are consistent with public vendor disclosures as of January 2026. Nvidia's Quantum-3450 (800V CPO, 144 ports) begins sampling in late calendar 2025 with volume ramp in the first half of calendar 2026. Nvidia's Spectrum-X CPO (Ethernet, 512 ports) ramps in the second half of calendar 2026. Broadcom's Bailey-2 CPO switch enters volume at Meta in the second half of calendar 2026. AWS and Google are expected to evaluate CPO in 2027 for their internal ASICs. By our base case, CPO ports reach roughly eight million per year in 2027 and twenty million per year by 2028, each consuming two to four external laser modules.

Two sensitivities matter. If CPO ramps faster than our base case (more AWS and Google internal ASIC adoption in 2027 rather than 2028), laser-module revenue is pulled forward by a year and Lumentum's FY28 earnings power rises by approximately $1.60 per share. If CPO ramps slower (delays on Nvidia Quantum-3450 at TSMC, or reliability concerns at a major customer), pluggable demand absorbs more of the bandwidth, which is also a Lumentum revenue line. The business is therefore positioned such that the company benefits in either path. The thing we do not see in any reasonable scenario is a world in which optical bandwidth growth slows materially; that scenario requires the AI CapEx cycle itself to break.

Our base case models 55 percent Lumentum share of external laser sources into CPO. We think this is conservative. Coherent is qualified and ramping, but Coherent also has significant telecom exposure that will absorb a portion of its indium phosphide wafer capacity. If Coherent's datacom allocation is constrained by its own telecom order book, Lumentum's effective share of incremental CPO laser demand could be 65 to 70 percent for the first two years of ramp. Any hyperscaler-driven move to lock in strategic supply commitments in the optics ecosystem, which we do not view as priced in, would further hardwire this share structure.

Channel Checks and Order Book

Our conviction on the revenue trajectory is supported by a set of channel checks we have done against the module integrator layer (Innolight, Fabrinet, Eoptolink), the test and inspection layer (Teradyne, KLA), the substrate layer (Sumitomo, IQE), and two of the hyperscalers directly. Five concrete observations from those checks materially de-risk the model.

First, lead times on EML chips have extended from twelve weeks in early calendar 2024 to twenty-eight to thirty-six weeks as of December 2025. This is a classic supply-constrained signature. Lumentum's bookings exceed its shipments by a ratio we estimate at 1.3 to 1.5 times over the last three quarters, and the order book now extends through calendar 2026. Module assemblers report that Lumentum has begun to allocate capacity to preferred customers rather than accepting new orders from all comers, which is consistent with a pricing environment that favors the supplier.

Second, Lumentum's selling price per EML chip rose by approximately 18 percent year over year in fiscal FY25, based on our estimate triangulated from reported revenue per chip and third-party BOM analysis of 800G and 1.6T transceivers. In a normal semiconductor cycle, rising volumes are accompanied by falling ASPs. The combination of rising volumes and rising ASPs is what the industry looked like during the HBM shortage of 2024-2025, and it is what it looks like now for 200G-per-lane EMLs.

Third, the OCS order book has broadened beyond Google. We have triangulated through three independent channels that Microsoft has placed a multi-quarter order for OCS components as part of its internal Hebron fabric, that Meta is evaluating OCS for its AI-specific fabric and has issued a qualification order, and that a third Tier-2 cloud is in evaluation. The $400 million disclosed backlog is, in our view, entirely real and a floor rather than a ceiling, because none of these qualifications have yet converted into multi-year supply agreements.

Fourth, Nvidia's CPO supply chain selection appears to be stable. Our checks suggest that the Quantum-3450 external laser module qualification was completed in November 2025 with two vendors (Lumentum and Coherent) and that the allocation of first-wave production has favored Lumentum by a margin of roughly 55 to 45 percent by unit volume. We expect to see further qualification testing at Spectrum-X CPO in the first half of calendar 2026 with the same two-vendor structure.

Fifth, the telecom and industrial legacy business has stabilized. After two years of declines, Lumentum's telecom and industrial laser business appears to have bottomed in calendar Q3 2025 and is growing modestly on a year-over-year basis, driven by 5G-Advanced build-out in India and industrial materials-processing demand. This is not the story, but it removes a meaningful source of consensus concern about the legacy drag.

At OFC 2025 in San Francisco, the laser-supplier booths ran out of engineering datasheets on the first day. Both Lumentum and Coherent had customer meetings scheduled back-to-back through Thursday. An engineering contact at one of the top-three hyperscalers described the laser allocation conversation with Lumentum's sales team as "borderline uncomfortable in the other direction." That is the sound of pricing power.

Revenue Build FY24 to FY28

Our quarterly revenue model for Lumentum is built bottom up, franchise by franchise. We model EML chip revenue as a function of unit shipments by lane-speed generation (100G, 200G, 400G) multiplied by ASP per lane, with assumptions for each. We model CPO laser-source revenue as a function of CPO port shipments multiplied by laser modules per port multiplied by ASP per module. We model OCS revenue as a ramp based on the disclosed backlog plus our channel-check estimates for additional order flow. The legacy telecom, industrial, and consumer (3D sensing) lines are modeled with modest growth around trend.

| $ millions | FY24A | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|---|

| Datacom EML / laser chips | 620 | 1,240 | 1,920 | 2,720 | 3,280 |

| CPO laser sources (ELS) | 0 | 35 | 180 | 620 | 1,180 |

| Optical circuit switch (OCS) | 0 | 20 | 85 | 280 | 545 |

| Telecom, industrial, consumer | 660 | 540 | 480 | 500 | 525 |

| Total revenue | 1,280 | 1,835 | 2,665 | 4,120 | 5,530 |

| YoY growth | -8% | +43% | +45% | +55% | +34% |

| Non-GAAP gross margin | 31% | 36% | 40% | 43% | 45% |

| Non-GAAP op. margin | 8% | 15% | 22% | 26% | 28% |

| Non-GAAP EPS ($) | 1.35 | 3.40 | 6.85 | 12.60 | 18.40 |

The step function in non-GAAP operating margin is worth emphasizing. Margins rise from 8 percent in FY24 to 28 percent in FY28 in our base case, a 2,000 basis-point expansion that comes from three distinct sources. Gross-margin mix shift (OCS and CPO laser are both above corporate average) contributes roughly 600 basis points. Operating leverage on the fixed cost base (Lumentum's R&D line does not grow proportionally with revenue because the IP base is largely in place) contributes roughly 900 basis points. ASP improvement on EML chips, which we assume persists through FY27 and then normalizes, contributes roughly 500 basis points. The leverage is real and is a critical part of the valuation story.

Valuation: DCF, Reverse DCF, and Sum-of-the-Parts

Valuation is where the thesis becomes easy to defend. Lumentum trades today at $228, which implies a market capitalization of roughly $15.8 billion and an enterprise value of roughly $14.6 billion (net of approximately $1.2 billion of net cash). Against our FY27E non-GAAP EPS of $12.60, that is an 18x forward earnings multiple on an asset whose earnings are growing at a compound rate above 50 percent. Against FY28E EPS of $18.40, that is 12.4x. Neither multiple is consistent with the underlying growth profile.

Discounted Cash Flow

Our DCF uses a ten-year explicit forecast, a 9.0 percent discount rate (reflecting the cyclical nature of the business), and a 3.0 percent terminal growth rate. The explicit forecast assumes revenue grows from $1.8 billion in FY25 to approximately $8.9 billion in FY35 as CPO and OCS mature, with operating margins stabilizing at 28 percent. Free cash flow reaches $2.3 billion in FY30 and $2.8 billion in FY35. The DCF output produces a per-share fair value of $485 as of end-2025, against a current price of $228. Sensitivity testing confirms the answer is robust: at a 10 percent discount rate and 2 percent terminal growth (a deliberately conservative combination), the DCF still produces $390 per share.

Reverse DCF

A reverse-DCF framing is even starker. At the current price of $228 and a 9 percent discount rate, the market is implicitly pricing Lumentum to grow revenue at roughly 12 percent per year for five years and then decline to GDP growth. For a business that delivered 43 percent revenue growth in the most recent fiscal year, is guiding +56 percent for the current quarter, and whose backlog implies continued acceleration, that implied trajectory is economically incoherent. The market is either not believing the guidance or extrapolating the 2019-2023 cyclical dynamics onto what is now a structurally different business.

Sum of the Parts

The sum-of-the-parts triangulates the DCF within a narrow range. We value each franchise on the multiple that its competitive intensity and growth profile warrant, and we net back the corporate-level adjustments. The output is an equity value of $460 per share, which is consistent with the DCF output within a reasonable margin.

The multiples we apply are defensible when set against peers. Our 6.5x FY28 sales multiple on the datacom EML franchise is below the 8-10x range at which Credo Semiconductor and Astera Labs trade on comparable profitability. Our 9x on the CPO franchise reflects its narrower competitive dynamics and higher incremental margin. Our 11x on OCS reflects the sole-source nature of the product and the hyperscaler customer structure. The weighted-average forward multiple on the total business, at $460 per share, is approximately 25x FY28E EPS, which is consistent with specialty semiconductor peer trading during periods of unit-volume growth in excess of 30 percent.

Bull, Base, and Bear Scenarios

Probability-weighted, the expected return to our $420 twelve-month PT is approximately 84 percent, and the expected return to our $640 twenty-four-month PT is approximately 180 percent. The asymmetry is the point of the trade: the bull and base cases combined carry 85 percent probability weight, and even the bear case implies a drawdown of only 25 percent from current spot, which is narrower than the downside on the typical cyclical semiconductor name. The risk-reward is attractive in a way that is specific to the single-name setup rather than generic to the AI theme.

Competitive Landscape

The usable competitive set is narrow, which is itself the thesis. A handful of companies are credibly addressing the laser and optical-engine layers of the AI optics stack, and their positioning relative to Lumentum determines whether the share-shift story is a one-way compounding or a two-way negotiation.

The only credible second source for EML chips and CPO laser modules. Broader portfolio than Lumentum (materials, industrial lasers, fiber-optic amplifiers), which both diversifies and dilutes the AI-optics exposure. Any major customer-driven strategic realignment in the optics supply chain would reshape the competitive structure, but none is visible in public disclosures as of January 2026. We prefer Lumentum for the purer exposure.

Contract manufacturer of optical modules for Nvidia, Ciena, and others. Not a laser maker. Fabrinet's business is a derivative of the same AI optics wave but captures less margin per unit. Relevant as a read-across signal: Fabrinet's forward guide is a leading indicator for the module-assembler layer but not for the laser-supplier layer.

Intel has an internal silicon photonics franchise built around its own DFB lasers and hybrid-bonded PICs. Primarily sells to select hyperscalers for internal use. Not a merchant supplier to the broader ecosystem, and the business has been slow to ramp. Monitoring for any merchant pivot but not modeling disruption.

Retail-led narratives with limited engineering substance and no volume production. Even specialist analysts who are positive on the CPO theme (Irrational Analysis, most notably) explicitly flag these names as “do not touch.” We avoid.

Dominate the 800G and 1.6T pluggable module assembly market. They buy EMLs from Lumentum and Coherent. Their growth is a co-indicator of Lumentum growth rather than a substitute. Export-control risk is real for Accelink but not for Innolight or Eoptolink based on current BIS framework.

Japanese III-V specialists supply indium phosphide substrate and, in some cases, laser chips to third parties. Mitsubishi has a direct-supply EML business, mostly into the Japanese telecom ecosystem. Not a structural threat to Lumentum's datacom share, but worth monitoring if they pivot more aggressively toward AI.

Risk Matrix

A 20 percent cut in 2026 hyperscaler CapEx would reduce optics order flow by roughly 25 percent. Mitigating: current guidance from Microsoft, Google, Amazon, and Meta points to combined 2026 CapEx above $700B, up from $580B in 2025. The guidance-setting rhythm suggests 2026 numbers are already baked, with risk skewed to the upside from new AI model releases rather than to the downside.

Top-five customers account for approximately 68 percent of revenue, dominated by Innolight, Eoptolink, Fabrinet, and two direct hyperscaler relationships. A qualification failure or share loss at any one could drive a single-quarter revenue miss of 8-12 percent. Mitigating: the qualification process is multi-year and sticky, and share is diversifying as OCS and CPO ramp.

Nvidia has the capital and engineering talent to bring CPO laser design in-house. It has not done so. Lumentum and Coherent are designated Tier-1 suppliers, and recent market speculation around strategic stakes in the optics ecosystem, if realized, would further cement the partnership model. We model no in-sourcing risk through FY28.

The 18 percent YoY ASP expansion observed in FY25 will not persist indefinitely. Our model assumes stable pricing through FY27 and mid-single-digit annual declines thereafter, consistent with historical datacom component cycles. A faster normalization (double-digit decline in FY26 rather than FY28) would trim 6-8 percent off our FY28 EPS.

The single biggest tail risk specific to the CPO franchise. A field-level reliability incident on a Nvidia Quantum-3450 CPO switch that traces to the laser module would damage Lumentum's brand and could delay the broader CPO ramp. Mitigating: Broadcom Bailey field data (50M test hours, zero failures) and Lumentum's extensive subsea-laser reliability record both suggest this is unlikely. The engineering physics of the laser modules is well understood.

U.S. export controls on high-performance optics remain limited to specific end-uses (military, certain state-backed telecom operators). Lumentum's hyperscaler-facing datacom and CPO business sells through U.S. and Taiwanese assembly, not directly to China, so direct export-control exposure is minimal. The secondary risk is through Chinese module assemblers (Eoptolink, Accelink) being restricted, which would affect module demand but not laser-chip shipments to non-Chinese assemblers.

The industry is structurally protected against new entrants. A III-V laser business requires a decade of epitaxy know-how, reliability data accumulated in customer deployments, and customer qualifications that take 12-18 months per socket. No credible new entrant is visible on the horizon. Watch Intel if Intel's silicon photonics business pivots merchant. We estimate probability at under 15 percent over three years.

The optics industry has historically cycled on two-to-three year rhythms. AI demand has flattened that cycle over the last two years, but a future cyclical downturn is inevitable. Our base case assumes a modest deceleration in FY29 (not modeled in the explicit forecast through FY28). The timing of the next cycle is the primary long-term risk to the multi-year thesis.

Catalyst Calendar 2026

The Lumentum story is narrative-rich and event-driven over the next twelve months. The catalyst set below is ordered by probability-weighted stock impact, in our estimation.

| Date (estimated) | Event | What to watch | Expected impact |

|---|---|---|---|

| Feb 2026 | Q2 FY26 earnings | Revenue vs $650M guide midpoint, Q3 guidance, CPO laser revenue disclosure | High positive if beat-and-raise |

| Mar 2026 | Nvidia GTC 2026 | CPO switch roadmap, any strategic supplier commentary, Rubin accelerator optics attach rate | Potentially high positive |

| Mar 2026 | OFC 2026 San Francisco | Lumentum technical disclosures on SLITE modulator, CPO laser reliability data, OCS roadmap | Medium positive, narrative support |

| May 2026 | Q3 FY26 earnings | CPO laser revenue step, OCS backlog updates, FY27 margin guidance | High positive if CPO inflects |

| Aug 2026 | Q4 FY26 earnings | FY26 close above $2.6B, FY27 initial guide | Medium-high positive |

| H2 2026 | Broadcom Bailey-2 volume at Meta | Second-hyperscaler CPO production deployment; laser-module order flow | Medium positive |

The Q2 FY26 earnings print in February is the single most important near-term catalyst. The company guided $650M for the quarter on the Q1 call. Our channel checks and order-book work suggest the number will land closer to $660-680M, with the CPO laser line reaching its first $40-50M quarter. That would be a 65 percent year-over-year revenue print with operating margins clearing 22 percent for the first time. The stock set-up into that print is not demanding; our base case assumes a reasonable beat-and-raise drives a 20-25 percent re-rating in the week of the print.

Our Call and Position Sizing

We are initiating Lumentum at Conviction Long with a 12-month price target of $420 (84 percent upside) and a 24-month price target of $640 (180 percent). We recommend the name as a top-three technology holding for the 2026-2027 window, sized at 4-6 percent of a diversified technology book for institutional risk tolerance. For dedicated AI-infrastructure books, sizing up to 8-10 percent is defensible given the quality of the franchise economics and the asymmetric risk-reward.

The single highest-conviction reason to own this name is that the thesis does not depend on a single technology winning, on a single customer remaining loyal, or on a single product cycle sustaining. It depends on the combination of three structurally scarce franchises (EML leadership, CPO laser duopoly position, OCS volume lead) whose aggregate growth is driven by the AI infrastructure build-out. If the build-out continues, Lumentum compounds earnings at 40 to 60 percent per year over the next three years. If the build-out decelerates, the legacy businesses (telecom, industrial, consumer) provide a floor and the franchise characteristics (2-vendor duopolies, long qualification cycles) limit the downside. There is no scenario we can construct in which the stock is worth less than 1.5x its current price on a three-year horizon, absent a macro-scale AI capex reset that would also reprice every other AI-exposed asset.

We would move to a less constructive rating on three conditions. First, a confirmed design-in loss at Nvidia CPO to a third vendor (other than Coherent) beyond the current two-source structure. Second, a change in Lumentum management that departed from the current engineering-led direction. Third, a sustained multi-quarter decline in EML unit volumes driven by a CPO ramp that is substantially faster than even our bull case (which would mean our revenue mix is wrong, not our total revenue outlook). None of these conditions are present as of January 2026.

The market's failure to price this name correctly is not because the thesis is hidden. The sell-side reports are public. The management commentary is public. The channel-check signals are available to anyone willing to make calls to the assembly layer. The failure is a classification failure: Lumentum is modelled as a cyclical datacom components supplier, which is a ten-year-old description that stopped being true in 2024. The market is waiting for a clearer signal, and our view is that the signal arrives with the Q2 FY26 print in February and compounds through GTC, OFC, and the first CPO revenue disclosures in spring. The window to own the name before the re-rating is closing, and we think it closes inside this calendar year.

Conclusion

Lumentum is the purest, narrowest, and most structurally advantaged public-market exposure to the AI optics build-out. It sits one layer beneath the module assemblers the market already owns, in a business with two credible competitors and a decade-long moat. The stock trades at 12x our FY28 earnings estimate, for a franchise growing earnings at 45 to 55 percent compounded. We initiate coverage at Conviction Long, with a 12-month price target of $420 and a 24-month price target of $640. The proximate catalyst is the Q2 FY26 print in February; the multi-year story is the CPO ramp from 2026 through 2028. In our view, the set-up offers one of the cleanest risk-adjusted return profiles in the AI infrastructure complex, and the opportunity to own the franchise ahead of the re-rating closes inside this calendar year.

About Glacium Research

Glacium Research is an independent institutional research firm covering semiconductors, AI infrastructure, and the optical interconnect supply chain. We serve portfolio managers, analysts, and allocators who require deep technical and financial analysis beyond what sell-side coverage provides. Our work combines primary-source engineering research, supply-chain channel checks, and rigorous valuation methodology, with a focus on names where the gap between engineering reality and market perception is widest.

Our guiding principles

- Engineering first. Technical fundamentals drive every investment view. We start from the physics and the manufacturing reality, then move to the financials.

- Genuine independence. No banking relationships, no issuer compensation, no sell-side distribution pressure. Our only clients are institutional subscribers.

- Conviction over coverage. We publish only on names where we have a differentiated edge, not a calendar of maintenance updates.

- Long-horizon orientation. Franchises are evaluated on three-to-five-year windows. Quarterly noise is context, not thesis.

- Transparent assumptions. Every model input, scenario probability, and channel check is sourced and auditable.

As of January 10, 2026

Disclosures

Analyst certification. The analyst responsible for this report certifies that the views expressed accurately reflect their personal views on the subject securities and issuers, and that no part of the analyst's compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in this report.

Positions. Glacium Research and its principals may hold long or short positions in securities discussed herein, including LITE, COHR, FN, and AI-semiconductor-related indices and ETFs. Positions may change without notice. Glacium Research does not receive compensation from any issuer of securities covered in its research, nor does it provide investment banking, corporate finance, or advisory services to such issuers.

Price targets, ratings, and scenario probabilities. Price targets, conviction ratings, and scenario probabilities represent the analyst's best-estimate view as of the publication date and are conditional on the assumptions detailed in the report. Actual outcomes may differ materially. Ratings are reviewed on a rolling basis and may be updated without prior notice.

Distribution. This material is issued by Glacium Research and is intended solely for institutional and professional investor use. It is not intended for, and must not be distributed to, retail investors. The information herein is furnished on a confidential basis; redistribution, reproduction, or resale, in whole or in part, is prohibited without prior written consent.

General information. The information in this report is believed to be accurate as of the date of publication, but no representation or warranty, express or implied, is made as to its accuracy or completeness. Nothing herein constitutes investment, tax, legal, or accounting advice, a solicitation to buy or sell any security, or a recommendation for any particular investor. Past performance does not guarantee future results, and forward-looking statements are subject to change without notice. Investors should conduct their own due diligence and, where appropriate, consult their own financial, tax, and legal advisors before acting on any of the views expressed in this report.

Image and data sources. Charts and exhibits reflect Glacium Research modelling, company filings (10-K, 10-Q, proxies), earnings call transcripts, conference disclosures (OFC, ISSCC, Hot Chips), and proprietary channel checks. Underlying data is available to institutional subscribers on request.

Copyright © 2026, Glacium Research. All rights reserved.GR-LITE-2026-01